The Future of Money: India or the West?

Is the Developing World Leading the Future of Payments?

Hi,

As a lifelong tech enthusiast with a passion for financial innovation, I've had the privilege of witnessing the fintech revolution unfold over the past two decades. From my early days coding in COBOL to co-founding SwiffyLabs, I've always been fascinated by the intersection of technology and finance. While my journey has primarily focused on lending technology, recent developments in the payments landscape have captured my attention and, frankly, blown my mind.

The intersection of lending and payments is becoming increasingly crucial, and as a leader in fintech, it's imperative to understand and anticipate these shifts.

A recent Bank of England paper highlighted something truly fascinating: India and Brazil are leading the charge in A2A (Account-to-Account) payment innovation, while the UK, despite being an early pioneer, is lagging behind. This revelation is mind-boggling, especially when we look at the numbers.

The tale of two payment systems

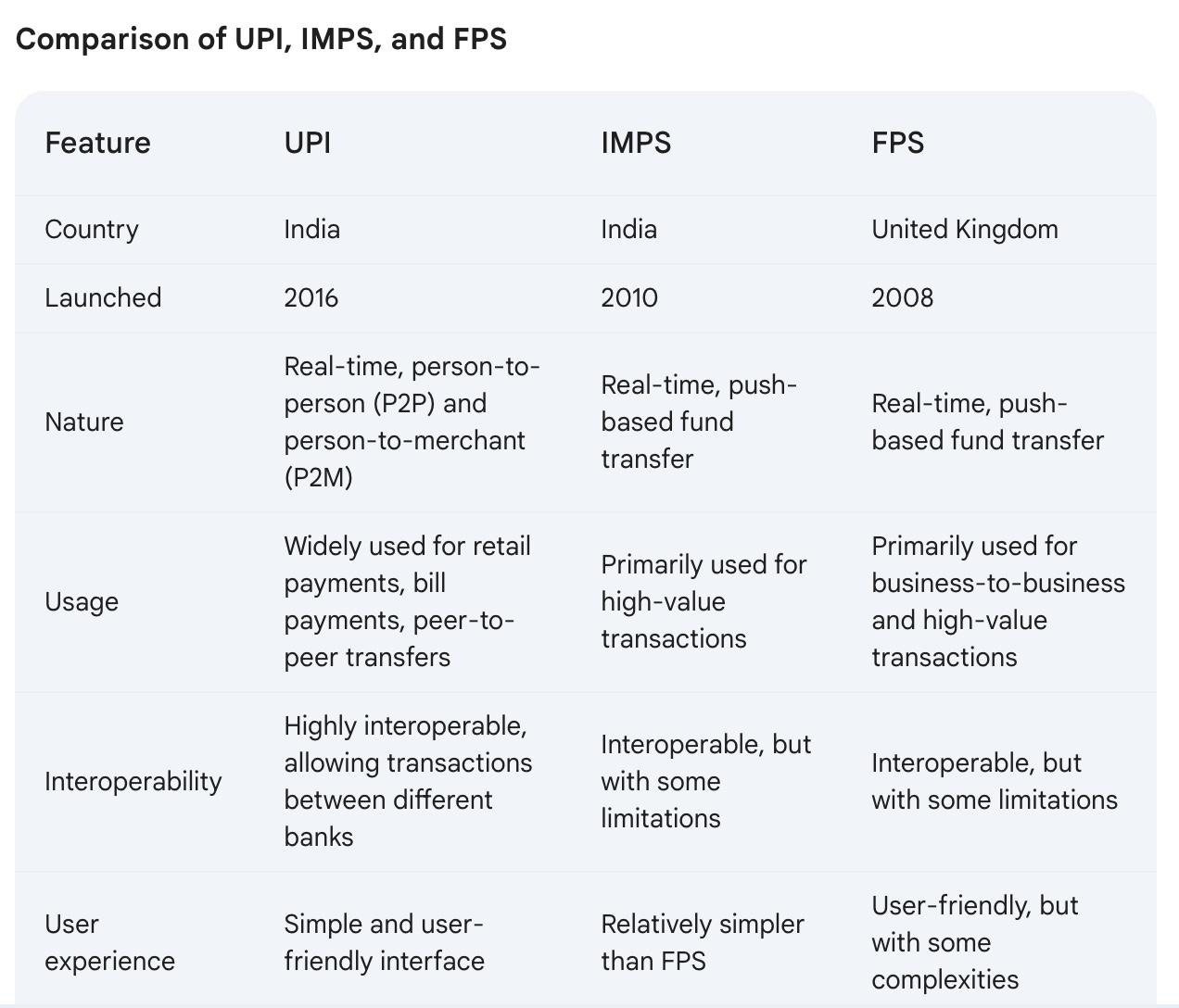

The UK's Faster Payments Service (FPS) and India's Unified Payments Interface (UPI) presents a fascinating case study in the evolution of digital finance. It's a story that challenges our preconceptions about technological adoption in developed versus developing economies.

The UK, traditionally seen as a financial powerhouse, was an early mover in the faster payments space. In 2008, it launched the FPS, pioneering real-time payments. However, recent data paints a picture of modest growth. According to a report by UK Finance, FPS accounted for just 10% of transactions in 2023, totaling 4.9 billion. The projection for 2033 - 7.2 billion transactions - suggests a steady but far from explosive growth trajectory.

What can the UK learn from India?

Now, let's shift our focus to India. The contrast is striking. India's Immediate Payment Service (IMPS), introduced in 2010, and the Unified Payments Interface (UPI), launched in 2016, have utterly transformed the country's payment landscape. In the 2023-24 financial year alone, IMPS handled 6.6 billion transactions, while UPI processed an astounding 131.13 billion. Combined, these systems accounted for 83.60% of retail digital payments in India. Even more remarkably, projections suggest India could reach 1 billion transactions per day within the next five years!

The success of UPI can be attributed to several key factors such as ease of use and accessibility, government and regulatory support, interoperability, cost-effectiveness for consumers and merchants, and robust security features.

Perhaps most tellingly, while the FPS implementation in the UK didn't significantly impact debit card usage, in India, IMPS/UPI has halved debit card transaction volumes in just four years! This shift underscores the transformative power of well-implemented faster payment systems.

This comparison raises a provocative question: Is the developing world outpacing the developed in digital payments? The evidence suggests so. India's experience demonstrates how real-time payments can drive financial inclusion and dramatically increase digital transaction volumes.

As a founder transitioning from a focus on lending to a broader view of financial technology, I find this paradigm shift both exciting and challenging. It underscores the importance of strategic initiatives, technological innovation, and fostering consumer adoption. More importantly, it suggests that we in the developed world might need to look to emerging economies for lessons in payment innovation.

The success of UPI offers valuable insights for countries like the UK. It's a reminder that innovation isn't always about being first, but about continuous improvement and adaptation. As we at SwiffyLabs work on our next generation of payment solutions, we're keeping a close eye on these global trends, learning from successes like UPI to create more efficient, inclusive, and transformative financial technologies.

In the race towards frictionless payments, it seems the developing world is setting the pace. It's time for established financial centers to take note and, perhaps, learn a lesson or two from India's payment revolution.

The journey from my early days of writing 800 lines of COBOL code to today's world of AI-driven, frictionless payments has been extraordinary. But I believe we're just at the beginning. The true revolution in finance is yet to come, and it's going to be powered by intelligent, seamless, inclusive, and secure payment systems.

As we stand on the brink of this new era, I'm more excited than ever about the possibilities ahead. The future of money is frictionless, intelligent, and incredibly promising. The question is, are we ready to learn from global innovators and lead the charge into this new financial frontier?

I’d love to know what you think!

Until next time,

Ashish